Introduction

Do you actually know what your business would sell for today — not what you paid to build it, not what it shows on your balance sheet, but what a qualified buyer would put on the table right now?

Most private business owners don't. Some overestimate by assuming years of hard work translate directly into dollars. Others underestimate and leave significant money on the table when it matters most.

Whether you're planning an exit, bringing on an investor, navigating succession, or just benchmarking where you stand, getting an accurate picture of your business's value in 2026 matters more than most owners realize.

M&A activity in the lower middle market remains active, buyer financing conditions are shifting, and an entire generation of business owners is approaching the transition window at the same time.

This guide covers what business valuation actually means for privately held companies, the methods used, the key drivers that push value up or pull it down, and the practical steps you can take now to improve your outcome.

Key Takeaways

- Business valuation uses financial analysis and market data to determine what your company would sell for to a willing buyer

- Multiple valuation methods exist — EBITDA multiples, DCF analysis, and asset-based approaches — chosen based on your business's financial profile

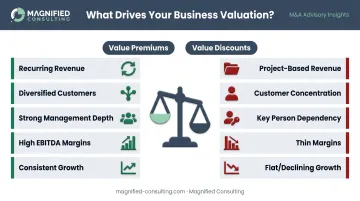

- Intangible factors like recurring revenue, management depth, and customer diversification drive significant premium or discount

- The best time to get a valuation is 2-3 years before a planned sale, not the week you decide to list

- Engaging an advisor 12-24 months before going to market can directly increase your final sale price

Why Business Valuation Matters for Private Business Owners in 2026

The Triggers Are More Common Than You Think

Owners seek formal valuations for reasons beyond a pending sale. The most common triggers include:

- Exit and sale preparation — establishing a realistic asking price and identifying value gaps before going to market

- Bringing in a partner or investor — ensuring equity is priced fairly from the start

- Buy-sell agreement disputes — when partners disagree on what the business is worth

- Estate and succession planning — particularly for family-owned businesses transitioning leadership across generations

- SBA loan applications — certain financing situations require independent business valuations

These triggers are hitting all at once. According to the Exit Planning Institute, 51% of American businesses are currently owned by Baby Boomers, and most are expected to transition ownership within the next decade. That's an enormous wave of privately held companies entering the market — many of which have never had a formal valuation.

The market is already responding. BizBuySell reported 2,345 small businesses sold in Q1 2026, with a combined $2B in enterprise value. Manufacturing acquisitions rose 16% year over year in the same period.

Book Value vs. Market Value: A Critical Distinction

Your balance sheet shows what you own minus what you owe — but it doesn't show what a buyer will pay.

For most privately held businesses, a substantial portion of value lives in intangibles that never appear on a balance sheet:

- Customer relationships built over years in a local market

- A reputation that drives repeat business and referrals

- Proprietary processes that improve margins or reduce lead times

- A management team that operates without the owner present every day

All of it affects the price a buyer will pay. Market value reflects what a qualified buyer — with access to your financials and market context — would actually offer. That number can be considerably higher or lower than book value, depending on how your business is structured.

Key Factors That Determine Your Business's Market Value

Revenue Quality and Predictability

Buyers pay premiums for businesses where next year's revenue is predictable. A construction firm with three long-term municipal service contracts looks very different to a buyer than one that bids competitively on every job.

Contract-based revenue — retainers, service agreements, and subscription-style arrangements — reduces buyer risk, and lower risk translates directly into higher multiples. If your business relies heavily on one-time project revenue, transitioning even a portion to recurring arrangements before a sale can meaningfully lift your final valuation multiple.

Customer Concentration Risk

A common M&A guideline: no single customer should represent more than 10% of revenue. At the 10-20% range, buyers start treating it as moderate concentration risk. Above 20% from one client, most acquirers apply a discount, sometimes a steep one.

If your top customer walks out the door after the acquisition, what happens to the cash flows the buyer just paid for? That uncertainty gets priced directly into the offer.

A diversified client base across multiple industries and revenue sizes signals stability and reduces that discount.

Management Depth and Key Person Risk

When you're the primary relationship holder, lead decision-maker, and face of the business, buyers will apply a key person discount. It's one of the most common value suppressors in privately held companies — and one of the most fixable.

Buyers pay more for businesses that run as systems, not personalities. A strong management structure typically includes:

- Department heads who manage their own teams independently

- Client relationships distributed across sales and account management staff

- Documented processes that guide operations regardless of who's in the building

Building that structure before a sale is foundational. Buyers want assurance the business runs without the owner — and they'll pay for that confidence.

Operational Efficiency and Profit Margins

EBITDA margin — earnings before interest, taxes, depreciation, and amortization, expressed as a percentage of revenue — is the most widely used measure of a business's operational health in M&A. Higher margins reflect pricing power, cost discipline, and operational efficiency. They also attract higher multiples.

Two businesses with identical revenue but different EBITDA margins will not receive identical offers. The higher-margin business signals a more efficient operation, which reduces execution risk for the buyer.

Growth Trajectory and Market Position

Consistent year-over-year revenue growth tells a buyer the business has real momentum, not a one-time spike. Pair that with a defensible market position, and you have the profile that commands premium multiples. Defensible positions typically come from niche expertise, regional brand recognition, or a proprietary process competitors can't easily replicate.

In 2026, certain industry tailwinds are providing additional lift. Construction businesses tied to infrastructure spending, technology-adjacent professional services firms, and manufacturers serving high-growth sectors are all benefiting from favorable market positioning that buyers factor into their offers.

Business Valuation Methods: Which Approach Fits Your Business?

No single method fits every situation. The right approach depends on the company's size, financial maturity, industry, and the purpose of the valuation.

Revenue Multiple Method

The revenue multiple is the most accessible starting point for small-to-mid-sized private businesses, particularly when earnings are volatile or the company is in a growth phase where profitability hasn't yet caught up with top-line expansion.

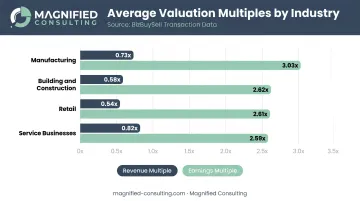

The formula is straightforward: annual revenue multiplied by an industry-specific factor. According to BizBuySell transaction data, average revenue multiples across industries range from roughly 0.54x to 0.82x for small businesses, with variation by sector:

| Industry | Avg. Revenue Multiple | Avg. Earnings Multiple |

|---|---|---|

| Manufacturing | 0.73x | 3.03x |

| Building & Construction | 0.58x | 2.62x |

| Retail | 0.54x | 2.61x |

| Service Businesses | 0.82x | 2.59x |

Revenue multiples are a useful starting point, but they don't account for profitability — two businesses with the same revenue but very different cost structures will look identical under this method.

EBITDA Multiple Method

That profitability gap is exactly what the EBITDA multiple addresses. For businesses with stable, predictable earnings, it's the preferred benchmark — accounting for cost efficiency and giving buyers a clearer picture of what they're actually acquiring.

For smaller businesses (under $2M in value), cash-flow/SDE multiples from BizBuySell average around 2.6x-3.0x depending on industry. In the lower-middle market ($5M-$50M), IBBA/M&A Source data shows median EBITDA multiples reaching 6.0x in Q3 2025 — and 61.9% of dealmakers expect multiples in this range to remain stable through 2026.

Discounted Cash Flow (DCF) Analysis

DCF projects your future cash flows and discounts them back to present value using a risk-adjusted rate. The discount rate reflects the risk a buyer perceives in those future earnings — higher uncertainty means a higher rate, which reduces present value.

DCF is best suited for businesses with reliable, forecastable cash flows. It requires defensible financial projections and solid historical data. For owner-operated businesses with variable earnings, it's typically used alongside — not instead of — multiple-based methods.

Asset-Based Valuation

This method calculates business value as total assets minus total liabilities. It's most relevant for asset-heavy businesses — manufacturers with significant equipment, construction firms with owned home services businesses — and typically produces the most conservative baseline.

For going-concern businesses where value is tied to earnings, workforce, and customer relationships, asset-based valuation alone will understate market value. It's most useful as a floor figure or in distressed scenarios.

How to Strategically Build Business Value Before a Sale

The most impactful value-building work happens 12-24 months before a sale — not in the final weeks before listing.

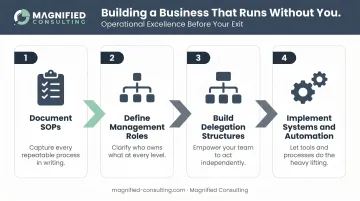

Systematize and Document Operations

Buyers are purchasing a business that will keep generating returns after they take over. The more clearly that business can operate without the founder, the more confident — and generous — a buyer will be.

Practical steps:

- Document standard operating procedures for all core functions

- Define management roles and decision-making authority in writing

- Build delegation structures so operational decisions don't funnel through the owner

- Implement systems and automation that reduce reliance on institutional knowledge held by one person

Magnified Consulting works with business owners across manufacturing, construction, retail, and professional services to build these structures — covering process reengineering, leadership development, and succession planning — with the goal of reducing key person risk before a transaction.

Diversify Your Customer Base and Build Recurring Revenue

Customer concentration and revenue predictability are two of the first things buyers scrutinize. These moves address both directly:

- Add clients across different industries and revenue tiers — reducing the percentage any single customer represents

- Transition project-based work to retainer or contract arrangements where possible — even partial conversion signals more predictable future cash flows

Cleaner financials make the next step — presenting those numbers convincingly — far more straightforward.

Improve Financial Health and Clean Up the Books

Clean, well-documented financials accelerate buyer confidence and reduce friction in due diligence. Specifically:

- Normalize owner compensation — separate personal expenses from business expenses clearly

- Document non-recurring expenses — one-time costs that won't repeat should be identified so buyers can see true run-rate EBITDA

- Prepare for a Quality of Earnings (QoE) review — most M&A transactions price at a multiple of adjusted EBITDA, and a QoE analysis validates that figure for buyers

Working with an experienced consulting partner before going to market can help identify these gaps early. Magnified Consulting's pre-transaction work — shaped by Mark Elender's involvement in over $1.5 Billion in M&A transactions — targets the operational gaps and profitability metrics that determine whether a business commands a premium or leaves money on the table.

When to Work with a Business Valuation Consultant

DIY Estimate vs. Professional Valuation

A rough estimate using published industry multiples and your own financials can give you a directional number. That's useful for early planning but insufficient for transactions.

Situations requiring a formal professional valuation:

- Business sale or acquisition transactions (particularly over $1M)

- SBA financing applications

- Estate and gift tax planning

- Litigation, partner disputes, or buy-sell agreement triggers

If you're still in the planning or value-building phase — not yet ready to go to market — a consulting-supported market analysis is often the better starting point. It identifies the gap between current value and target value, and provides a roadmap for closing it.

What to Look for in a Valuation Advisor

Not all valuation professionals serve the same purpose. Key selection criteria:

- Industry experience — an advisor familiar with your sector will apply realistic comps, not generic benchmarks

- Real transaction experience — understanding what buyers actually pay, not just what accounting formulas produce

- Forward-looking guidance — the goal isn't just a number, it's a strategy for improving that number

- M&A advisory track record — exposure to actual deal flow is irreplaceable when advising on positioning and pricing

Magnified Consulting's partners have collectively been involved in over $1.5 Billion in M&A advisory work — the kind of real deal exposure that shapes how they evaluate a business's market position, not just its accounting value.

Credentials to Know

For formal certified appraisals, look for these designations:

- CVA (Certified Valuation Analyst) — issued by NACVA

- ABV (Accredited in Business Valuation) — issued exclusively by the AICPA

- ASA (Accredited Senior Appraiser) — issued by the American Society of Appraisers

- CBA (Certified Business Appraiser) — a legacy IBA/NACVA credential

A certified appraiser is necessary when a defensible, credentialed valuation report is required — for litigation, estate tax filings, or formal financing. For owners focused on building value and understanding what the market will actually pay, an experienced M&A advisor delivers more actionable guidance than a credentialed appraisal alone.

Frequently Asked Questions

What is a business valuation consultant?

A business valuation consultant is a professional who determines a business's economic value using financial analysis, market data, and industry benchmarks. They support M&A transactions, exit planning, estate planning, and strategic financial decisions for business owners.

How do I know what my business is worth in 2026?

Business value is determined by applying the appropriate valuation method — revenue multiples, EBITDA multiples, or DCF analysis — to your financials and comparing against comparable transactions. An experienced advisor benchmarks your numbers against real market data to ensure the result reflects current buyer expectations.

What valuation method is best for small and mid-sized private businesses?

Most private businesses under $50M in revenue are valued using revenue or EBITDA multiples as a starting point. DCF analysis is added for businesses with stable, predictable cash flows. The right approach depends on your financial maturity and the purpose of the valuation.

When is the best time to get a business valuation?

Get a valuation 2-3 years before a planned sale to allow time for value-building improvements. It's also useful at major milestones: taking on a partner, applying for financing, or beginning estate and succession planning.

How can I increase the value of my business before selling?

Focus on reducing customer concentration, building recurring revenue, and improving EBITDA margins — then document processes to reduce owner dependency. Engaging a consulting advisor 12-24 months before going to market, as Magnified Consulting does with exit-focused clients, gives you time to act on improvements that buyers actually pay for.

How long does a business valuation take?

Most professional valuations are completed in 2-6 weeks. Single-location businesses with clean financials often finish closer to 2-3 weeks; multi-entity or complex structures typically require additional time.