The gap between assumption and reality tends to surface at the worst possible moment: when a buyer shows up, a lender needs a figure, or a life event forces the question. By then, there's little runway to close it.

The difference between an average valuation and a well-prepared one can represent hundreds of thousands—sometimes millions—in exit proceeds. That gap is almost always driven by factors an owner could have addressed years earlier.

This guide covers the primary valuation methods used for IT services companies, the multiples buyers are paying in 2025–2026 by segment and company size, and the specific factors that move your number up or down.

Key Takeaways

- IT services companies are primarily valued on normalized EV/EBITDA multiples, with EV/Revenue used as a secondary cross-check

- Median EV/EBITDA for IT services M&A settled at 8.8x in Q4 2025, down roughly 20% from the 2021 peak of 10.7x

- Recurring revenue (managed services, long-term contracts) commands significantly higher multiples than project-based work

- Smaller deals under $5M trade at 5x–6x EBITDA; scaled platform companies reach 11x+

- Key person dependency, customer concentration, and undocumented processes are the top three valuation discounts

What Determines the Value of an IT Services Business

Why IT Services Businesses Are Valued Differently

IT services companies don't have factories, equipment fleets, or large inventory positions. Their value sits in client relationships, recurring contracts, proprietary processes, and the institutional knowledge of the people delivering the work. According to Ocean Tomo's 2025 Intangible Asset Market Value Study, intangible assets now constitute approximately 92% of S&P 500 market capitalization—up from just 17% in 1975. While that figure covers large public companies broadly, it reflects the same structural reality facing private IT services firms: the value is overwhelmingly intangible.

This creates a specific challenge for valuation. Standard asset-based methods—which tally up tangible assets minus liabilities—severely undervalue IT companies. Earnings-based and market-based approaches are far more relevant because they capture what buyers are actually acquiring: a revenue stream, a client base, and a repeatable delivery model.

SDE vs. EBITDA: Which Metric Applies to Your Business

Choosing the wrong profitability metric produces a meaningless valuation. The two most common profitability metrics serve different purposes:

Seller's Discretionary Earnings (SDE) adds back the owner's full compensation to net income, capturing total financial benefit to a single owner-operator. This is the standard metric for smaller IT firms—typically under $5M in revenue—where the owner is central to operations and service delivery.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) treats a normalized management salary as an operating expense rather than adding it back. Institutional buyers and private equity firms use this metric for larger businesses ($5M+ revenue) because it reflects what the business earns with professional management installed.

Applying EBITDA multiples to an SDE number produces an inflated—and misleading—valuation. Verify which metric applies to your business before any multiple is ever discussed.

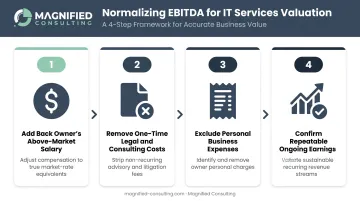

EBITDA should always be adjusted before applying multiples. Normalized EBITDA should reflect sustainable, repeatable earnings—what the business will actually generate under new ownership. Standard adjustments include:

- Adding back the owner's above-market compensation

- Removing one-time legal or consulting fees

- Stripping out personal expenses run through the business

IT Services Valuation Methods Explained

Three core approaches exist. Each serves a different purpose:

- Income-based: Projects earning power; the primary driver of value in IT services

- Market-based: Compares against recent transactions and public company data

- Asset-based: Establishes a value floor; rarely the primary method for service businesses

Most IT services valuations triangulate between income-based and market-based analysis, while treating asset-based results as a minimum benchmark.

The EBITDA Multiple Method

This is the dominant method for IT services companies:

Enterprise Value = Normalized EBITDA × Industry Multiple

IT services firms generate positive cash flow early, require minimal capital investment, and carry few physical assets. Profitability is the clearest signal of value, and EBITDA captures it cleanly.

A simple example: An IT services company with $3M in revenue and 13% adjusted EBITDA margins generates approximately $390,000 in normalized EBITDA. At a 10x multiple, the enterprise value is $3.9M. That multiple could compress to 6x for a smaller firm with key person risk, or expand to 12x for a managed services provider with high recurring revenue and strong retention.

The normalization process matters as much as the multiple:

- Add back the owner's above-market salary

- Remove one-time legal, consulting, or transition costs

- Exclude personal expenses run through the business

- Confirm the adjusted number reflects ongoing, repeatable earnings

The Revenue Multiple Method

Revenue multiples serve as a cross-check, not a primary method. They're most relevant when EBITDA is temporarily distorted by a heavy investment year, when the company is in a high-growth phase, or when comparing firms with different cost structures.

Current EV/Revenue ranges vary significantly by segment (covered in the next section). The broader IT services historical median sits around 1.3x, per Aventis Advisors data. What matters most here is revenue quality: recurring managed services revenue is worth considerably more per dollar than project revenue or resale revenue.

The Discounted Cash Flow (DCF) Method

DCF projects future free cash flows and discounts them to present value using a risk-adjusted rate. It works best for IT companies with sufficient operating history and predictable revenue streams—typically businesses with three or more years of consistent financials and a clear growth trajectory.

The practical limitation: DCF models are highly sensitive to growth assumptions and discount rate choices. A small change in either variable produces vastly different outcomes, which is why most IT services M&A transactions anchor on market-based multiples rather than DCF conclusions alone. DCF is most useful for internal planning or as a sanity check on those market-based results.

2026 IT Services Valuation Multiples: What the Market Is Paying

The 2021–2022 period was an outlier. Cheap capital, post-pandemic digital acceleration, and intense PE competition pushed IT services multiples to historic highs—EV/EBITDA peaked around 10.7x in 2021. Livingstone Partners' 2025 IT Services Market Overview confirms 2024 median EV/EBITDA fell to 8.8x, roughly 20% below that peak. The market has normalized, not collapsed. Owners who benchmarked their expectations against 2021 numbers need to recalibrate.

How Business Size Affects Your Multiple

Company size is one of the most powerful variables in IT services valuation. The spread between a small deal and a scaled platform company is significant:

| Deal/Company Size | Typical EV/EBITDA Range |

|---|---|

| Under $5M deal value / smallest MSPs | 3x–5.9x |

| Smaller add-on MSPs ($5M–$20M revenue) | 5x–8x |

| Mid-market MSPs ($20M–$50M revenue) | ~8.1x |

| Platform companies ($10M+ EBITDA) | ~11x |

Sources: Aventis Advisors MSP Valuation Multiples; Solganick Q3 2025 Technology Services M&A Report

The logic behind this spread: larger IT companies carry lower risk profiles, with more diversified client bases, deeper management teams, and the ability to serve enterprise accounts. They also attract more competitive buyer interest, particularly from PE platforms that have minimum deal size thresholds.

Solganick identifies platform MSPs at $10M+ EBITDA trading near 11x, while smaller add-on acquisitions typically trade at 5x–8x. PE bolt-ons reached 8.5 acquisitions for every platform deal in H1 2025, according to Corum Group data, reflecting intense demand for scale.

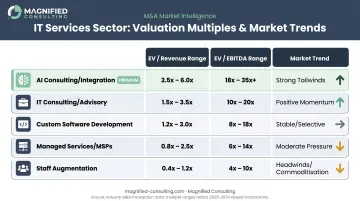

IT Services Multiples by Segment

The 2026 market is bifurcated. Segments tied to AI, cybersecurity, and cloud infrastructure are attracting premium buyer interest. Traditional project-based and labor-only models face headwinds as AI tools compress demand for certain types of work.

| Segment | EV/Revenue | EV/EBITDA | Trend |

|---|---|---|---|

| AI consulting / integration | 2.0x–4.0x | 12.0x–15.0x | Strong premium |

| IT consulting / advisory (specialized) | 1.6x–2.2x | 10.6x–13.0x | Premium for domain expertise |

| Custom software development | 1.5x–2.7x | 9.5x–12.2x | Stable for integrated teams; body-shop models discounted |

| Managed services (MSPs) | 0.9x–1.3x | 6.5x–12.0x | Highly scale-dependent |

| Staff augmentation | Not published | Not published | Qualitative headwinds from AI coding tools |

Source: Solganick Q3 2025 Technology Services M&A Report

Cybersecurity services M&A saw 111 deals in Q3 2025 alone, a year-over-year increase, reflecting strong buyer demand even without a published standalone multiple range.

AI has reshaped buyer expectations across the board. Firms that demonstrate AI consulting capabilities, proprietary implementation frameworks, or recurring managed services tied to AI infrastructure are commanding multiples at the top of the range. By contrast, traditional staff augmentation and time-and-materials development face pricing pressure as AI coding tools reduce the labor hours required to deliver the same output.

Key Factors That Increase or Decrease Your IT Services Valuation

Revenue Quality and Contract Structure

Not all revenue is valued equally. Monthly recurring revenue (MRR) under long-term contracts with auto-renewal provisions commands the highest multiples. Project revenue and transactional work trade at a discount because buyers cannot underwrite future cash flows with confidence.

Houlihan Lokey's December 2025 IT Services Market Update quantifies this gap clearly:

Houlihan Lokey's December 2025 IT Services Market Update quantifies this gap clearly:

| Business Model | EBITDA Multiple Range |

|---|---|

| Product-heavy VARs | 6x–7x |

| VARs shifting to managed services | 8x–9x |

| Service-focused companies | 10x–11x |

That 2.6x EBITDA multiple difference is driven almost entirely by revenue mix. The same report notes that 57% of VARs are adopting managed services capabilities specifically to capture this valuation premium.

Customer retention also matters. Aventis MSP data identifies retention above 90% as a stability signal that buyers reward in their offer prices.

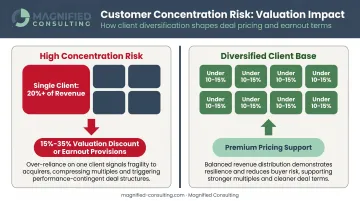

Customer Concentration Risk

A single client representing more than 20% of revenue is one of the most common deal complications in IT services M&A. According to general M&A advisory guidance from Icon Business Advisors, when one customer exceeds 20% of revenue, buyers may discount valuation by 15%–35% or restructure the deal with holdbacks or earnout provisions to offset the risk.

If that client leaves post-acquisition, the buyer has overpaid for a business that no longer exists in its underwritten form. A diversified base — where no single client exceeds 10–15% of revenue — eliminates this discount and supports premium pricing. Customer concentration is one of the fastest issues to address before going to market.

Key Person and Owner Dependency Risk

When the business's client relationships, technical expertise, or sales pipeline run through one individual—usually the owner—buyers discount accordingly. General valuation guidance from Andersen Global puts key person discounts in the range of 5%–30%, with ClearlyAcquired noting that founder-dependent businesses commonly see discounts around 15%–25% in M&A contexts.

Buyers look for specific indicators that a business can operate without its owner:

- Documented processes and service delivery runbooks

- A second tier of management with client-facing relationships

- Sales activity distributed across multiple team members

- Client contracts in the company's name, not the owner's personal relationships

How to Build Your IT Services Business Value Before a Sale

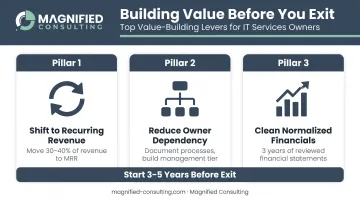

Valuation improvement is a multi-year effort, not a pre-sale sprint. The owners who extract the highest sale prices typically begin optimizing 3–5 years before an exit, working from a deliberate value creation plan rather than reacting to an opportunistic offer.

The three highest-impact levers for IT services owners:

Shift revenue mix toward recurring contracts. Managed services agreements with auto-renewal provisions directly increase the multiple buyers will pay. Even a partial shift—moving 30–40% of revenue to MRR—produces a meaningful valuation uplift.

Reduce key person and owner dependency. Document your processes. Build a second-tier management team. Distribute client relationships across multiple people. Every step that makes the business less dependent on you personally increases what a buyer is willing to pay.

Maintain clean, normalized financials. Three years of audited or reviewed financial statements with a clear EBITDA story removes buyer skepticism and supports a faster, cleaner transaction. Disorganized records create discount opportunities for buyers and slow deal timelines.

Engaging an exit strategy consultant well before the sale process starts dramatically changes outcomes. Magnified Consulting works with privately owned businesses across the Carolinas and Southeast on business valuation, financial performance optimization, and exit planning — helping owners understand where they stand today and what it takes to command a premium when they're ready to sell.

Frequently Asked Questions

How do you value an IT services company?

IT services companies are primarily valued using normalized EBITDA multiples, with EV/Revenue used as a secondary cross-check. The appropriate method and multiple depend on company size, revenue quality (recurring vs. project-based), and growth trajectory.

What is the Rule of 40 in tech valuation?

The Rule of 40 states that a software or SaaS company's revenue growth rate plus profit margin should equal or exceed 40%. It's primarily a SaaS benchmark. For IT services companies, buyers focus more directly on EBITDA margins, recurring revenue percentages, and how sticky the client base actually is.

What EBITDA multiple should I expect for my IT services business in 2026?

Multiples range from roughly 5x–6x for smaller deals to 11x+ for scaled platform companies, with the overall market median around 8.8x per Aventis Advisors Q4 2025 data. Segment, revenue quality, and company size all influence where you land within that range.

Does customer concentration affect my IT services company's valuation?

Yes—it's one of the most common valuation discounts. When a single client exceeds roughly 20% of revenue, buyers typically discount the valuation by 15%–35% or require earnout provisions to offset the risk of that client departing post-close.

What's the difference between SDE and EBITDA for IT business valuation?

SDE adds back the owner's full compensation and is the standard metric for smaller, owner-operated IT firms. EBITDA, by contrast, keeps a market-rate management salary as an operating expense — making it the appropriate benchmark once a business exceeds $5M in revenue and starts attracting institutional or PE buyers.

How does AI impact IT services business valuations in 2026?

The impact runs in two directions. Firms in AI consulting, cybersecurity, and cloud infrastructure are seeing stronger buyer demand and higher multiples — AI consulting is currently commanding 12x–15x EBITDA. Traditional staff augmentation and project-based development, however, face real pricing pressure as AI tools compress the labor hours needed to deliver the same output.