Introduction

Picture this: your operations team is buried in paper files, staff are manually cross-referencing documents, and client follow-ups are going out late — or not at all. Meanwhile, a competitor running automated workflows just responded to a client inquiry in under two minutes.

This isn't a hypothetical. It's the daily reality for many privately owned service businesses, and the operational drag is measurable. Industry research shows that the costs of manual processes across service companies have risen steadily since 2003, a trend that shows no sign of reversing. For businesses generating $10M or more in revenue, manual processes aren't just inefficient — they actively compress margins and erode customer loyalty.

This guide covers what business process automation actually means for service-based companies, which workflows to prioritize, the four stages of implementation, and the measurable benefits. It also explains why the consulting partnership behind the technology matters as much as the technology itself.

Key Takeaways:

- Claims, underwriting, renewals, and compliance are the highest-ROI automation targets

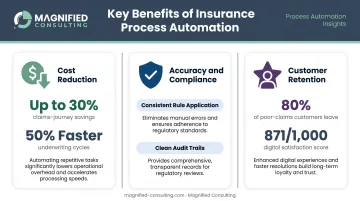

- Automation cuts claims-journey costs by up to 30% and halves underwriting cycle time

- Poor claims experiences drive 80% of dissatisfied customers to switch carriers

- A phased, consulting-led approach outperforms DIY tool deployment every time

- Ongoing mentorship after implementation is what makes automation deliver lasting results

What Is Business Process Automation in Insurance?

Business process automation (BPA) in insurance refers to using technology — including RPA bots, AI-driven workflows, and digital integration tools — to replace repetitive, rules-based human tasks across the insurance value chain. That spans everything from initial quoting and underwriting to claims adjudication and regulatory reporting.

Software Deployment vs. True Process Consulting

Buying automation software and implementing it effectively are two very different things.

Many agencies invest in tools and see disappointing results. The tools usually aren't the problem — the underlying workflows were never properly mapped, business rules weren't clearly defined, and staff were left to figure it out without structured support.

Effective automation requires:

- Upfront workflow analysis to identify where the real bottlenecks are

- Strategic sequencing of which processes to automate and in what order

- Integration planning across existing systems

- Change management to ensure staff adopt and sustain new workflows

That's the foundation of how Magnified Consulting approaches process optimization for business clients. Strategy and human alignment come first — before any technology is selected or deployed. That means starting with operational assessments and diagnostic tools to identify performance gaps and root causes, so automation decisions are grounded in what your business actually needs.

The result: automation investments that stick, because the groundwork was done right.

Key Areas Where Service Companies Should Automate First

Not everything should be automated at once. The highest-impact starting points share common traits: high transaction volume, clear rules-based logic, and significant manual time investment.

Client Intake and Request Processing

Client intake and request handling is often the most resource-intensive function in service businesses. Manual intake processes create bottlenecks, delays, and inconsistency that erode client satisfaction. Even incremental efficiency gains here carry outsized financial impact.

Automation can handle:

- Initial inquiry capture and routing to the right team member

- Document collection and verification against existing records

- Pattern-based triage and prioritization of incoming requests

- Status updates and follow-up communications without manual intervention

The payoff is real. Businesses implementing digital intake workflows consistently reduce response times and free staff from administrative work so they can focus on complex cases requiring human judgment.

Operational Processing and Approvals

Manual processing is slow and expensive. Staff often spend a significant portion of their time on non-core administrative tasks — data gathering, form completion, system entry — rather than actual value-adding work.

Automated processing systems pull from multiple data sources and dramatically compress turnaround times. Leading service companies have cut processing cycle times by 50% or more using digitized workflows. At scale, straight-through processing can handle a high percentage of standard transactions with no staff intervention required.

Contract and Renewal Management

Missed renewal windows and administrative errors erode retention rates in ways that compound over time. Research consistently shows that customers with poor service experiences are significantly more likely to leave — making renewal automation a direct retention lever.

Automating contract management addresses the root causes:

- Renewal reminders sent at the right time, through the right channel

- Documents generated and delivered without manual intervention

- Change requests processed without bottlenecking team workflows

Compliance and Regulatory Reporting

For privately owned businesses without large compliance departments, regulatory requirements across multiple jurisdictions create constant risk — especially in markets like the Carolinas and Georgia, where state-level licensing requirements and reporting deadlines differ significantly. License renewal deadlines, filing requirements, and audit documentation vary by jurisdiction and change regularly.

Automated compliance tracking:

- Monitors regulatory changes across operating jurisdictions

- Generates audit-ready documentation automatically

- Flags upcoming deadlines before they become penalties

Customer Service and Onboarding

Roughly 40% of inbound service calls are basic status checks, according to industry research. A well-configured automated workflow handles these without a team member picking up the phone.

Chatbots and automated intake tools manage routine inquiries and new client onboarding, freeing staff for conversations that actually require judgment and relationship-building.

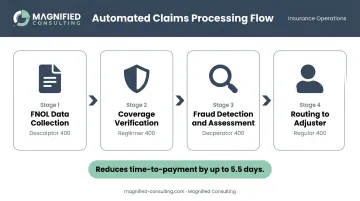

The 4 Stages of Process Automation for Service Companies

A structured, four-stage approach is what separates successful automation implementations from expensive experiments.

Stage 1 — Process Discovery and Assessment

Before any tool is selected, a thorough audit of current workflows identifies which processes are high-volume, error-prone, and time-consuming. That means understanding both the system side and the human side of operations — not just drawing process maps.

A consulting-led assessment is more thorough than an internal one. External consultants surface the gaps that staff have normalized and the workarounds that have become invisible. Magnified Consulting's approach uses diagnostic tools and stakeholder interviews to identify performance gaps and root causes of inefficiency — before any recommendations are made.

Stage 2 — Workflow Design and Planning

Stage 2 is where the strategic decisions get made:

- Which processes get automated first, and why

- What the automation logic and business rules look like

- Which tools fit the existing technology environment

- What success looks like and how it will be measured

Getting Stage 2 right prevents the most common failure mode: automating the wrong processes, in the wrong order, with the wrong tools.

Stage 3 — Implementation and Integration

Deploying automation tools into an existing service operation requires integration with legacy management platforms, CRMs, third-party data providers, and often multiple vendor systems. Of all four stages, this one demands the most technical precision — and it's where most DIY implementations break down.

Clean integration requires careful planning around data flows, system handoffs, and error handling. A half-integrated automation frequently creates new data silos instead of eliminating the old ones.

Stage 4 — Monitoring, Optimization, and Scale

Automation requires active management to deliver lasting value. Workflows need ongoing performance tracking against defined KPIs, regular refinement as business rules change, and a deliberate plan to expand into new operational areas over time.

Magnified Consulting's ongoing advisory model is built for exactly this stage — tracking performance against benchmarks, adjusting workflows as the business evolves, and identifying the next processes ready for automation.

Benefits of Automating Service Business Processes

Operational Cost Reduction

The financial case is well-documented. Automation can reduce claims-journey costs by up to 30%, according to industry research. At the underwriting level, automation eliminates the manual data-gathering burden that consumes nearly half of an underwriter's working day.

For a $10M+ agency, even a 15–20% reduction in operational costs represents hundreds of thousands of dollars in recaptured margin annually.

Increased Accuracy and Compliance Confidence

Manual data entry introduces errors, and errors in claims create disputes that cost money and erode trust. Automated processes apply rules consistently, create clean audit trails, and ensure compliance requirements are met uniformly, without relying on individual staff members to remember every step.

Faster Service and Improved Customer Retention

Speed matters more than most businesses realize. Research consistently shows that customers with poor service experiences are significantly more likely to switch providers. Automation enables faster resolution, instant responses, and around-the-clock service availability — each of which directly reduces churn.

The market is rewarding businesses that invest in faster, digital-first service. Customer satisfaction scores climb year over year for organizations that deploy well-configured automation across their client-facing workflows.

Scalable Growth Without Proportional Overhead

Once automation is in place, volume growth doesn't require headcount growth at the same rate. Research has found that businesses can handle significantly higher transaction volumes with no additional staff after implementing process automation. That's the operational capacity that makes growth financially sustainable.

Why Consulting Matters: Challenges Service Businesses Face During Implementation

Legacy System Complexity

Most independently owned service businesses run on systems built for a paper-driven world. Industry research notes that many legacy core systems create operating inefficiency and rising maintenance costs — and they weren't designed to integrate with modern automation tools.

Without careful ecosystem mapping before implementation, automation projects create new problems: data silos, workflow gaps, and reconciliation headaches between systems that don't communicate properly. An experienced consulting partner maps the full technology environment first.

Change Management and Staff Adoption

Most automation projects stall because of human factors, not technology failures. The most common culprits include:

- Unclear role changes that leave staff uncertain about their responsibilities

- Inadequate training on new workflows and tools

- Employee resistance rooted in fear of displacement

Industry surveys found that 53% of L&A core modernization respondents cited high project costs, and 47% cited talent impacts as major implementation risks.

This is where Magnified Consulting's long-term mentorship model creates real differentiation. Rather than handing off a deployed system and walking away, we stay engaged — working alongside operational leaders to ensure new workflows are adopted, refined, and sustained.

Clients have seen operational cost reductions of up to 30% and meaningful profitability improvements within the first six months. That outcome requires sustained advisory support, not a one-time implementation.

Choosing the Wrong Automation Scope

Trying to automate everything simultaneously is one of the most common mistakes privately owned businesses make. The result is a sprawling project with delayed ROI, frustrated staff, and unclear accountability.

A tailored consulting strategy — built around the specific operations of your business, not a generic enterprise template — identifies the two or three workflows where automation will deliver measurable impact fastest. Those early wins build organizational confidence and create the foundation for scaling automation into additional areas.

Frequently Asked Questions

What is a business automation consultant?

A business automation consultant analyzes your current workflows, identifies which processes are strong candidates for automation, and helps you select and implement the right tools. They also provide ongoing support to ensure the changes deliver measurable operational and financial results — not just a clean launch.

What is RPA in a service business?

RPA (Robotic Process Automation) uses software bots to handle repetitive, rules-based tasks — such as data entry, client intake, contract renewals, and compliance checks — that previously required manual effort. It frees staff to focus on complex, judgment-intensive work that automation can't replace.

What are the 4 stages of process automation?

The four stages are: Process Discovery and Assessment, Workflow Design and Planning, Implementation and Integration, and Monitoring, Optimization, and Scale. Each stage builds on the previous one. Skipping ahead is one of the most common reasons implementations fail.

Which business processes are best suited for automation?

The top candidates are client intake processing, approvals and data collection, contract renewals, compliance reporting, and routine customer service interactions. All are high-volume, rules-based processes where speed and accuracy directly affect profitability and retention.

How long does it take to implement process automation in a service business?

Timelines vary by complexity, but many businesses can deploy initial automations within a few weeks to a few months. A phased approach — starting with one or two high-impact workflows — produces faster results and clearer ROI than attempting a broad rollout from the start.