The research is more definitive than many expect. A 2026 literature review by Broadleaf Capital International examined 212 papers covering 285 findings on ERM and firm performance. 68% of findings showed a positive relationship between ERM and firm value. Only 4.5% showed negative outcomes.

That's not a blanket guarantee — the quality of implementation matters enormously, and the evidence is largely associative rather than strictly causal. But for privately owned and family-run businesses generating $10M or more in revenue, the case for structured risk management is compelling and worth understanding clearly.

This article translates that evidence into practical insight: what ERM actually is, how it creates value, when it fails, and what it looks like for a business your size.

Key Takeaways

- 68% of findings across 212 studies link ERM to improved firm performance — but implementation quality determines whether you see results

- ERM creates value through five mechanisms: reduced capital costs, earnings stability, stronger decisions, stakeholder confidence, and operational efficiency

- Checkbox ERM (appointing a risk officer without integrating risk thinking into decisions) produces costs without benefits

- ERM benefits compound over time; early-stage programs show modest results that grow as the framework matures

- Privately owned businesses can implement scalable ERM without a dedicated CRO, directly building enterprise value ahead of a sale or capital event

What Is Enterprise Risk Management (And How Is It Different from Traditional Risk Management)?

Traditional risk management works in silos. Your CFO manages financial exposure. Your operations team handles safety compliance. Each function addresses its own slice of risk, but no one connects them to how the business makes decisions or grows.

ERM is different. The COSO 2017 framework defines ERM as "the culture, capabilities, and practices integrated with strategy-setting and performance that organizations rely on to manage risk in creating, preserving, and realizing value." In other words, ERM isn't an add-on to operations. It's a management discipline embedded in how you run the business.

How ERM Connects Risk to Strategy

In practice, ERM means:

- Identifying the risks most likely to disrupt revenue or reduce business value — before they emerge

- Embedding risk awareness into decisions about hiring, capital allocation, geographic expansion, and new customer relationships

- Building a consistent view of risk exposure across the entire organization, not just one department

The Frameworks Behind ERM

Understanding what ERM does in practice is one thing. Knowing how to structure it is another. Two frameworks dominate how organizations build their ERM programs:

- COSO ERM (2017): Organizes ERM around five components — Governance and Culture; Strategy and Objective-Setting; Performance; Review and Revision; and Information, Communication, and Reporting

- ISO 31000:2018: Defines risk as "the effect of uncertainty on objectives" and emphasizes integration, leadership commitment, and continual improvement

Neither framework requires a large team or a dedicated risk department. Both require genuine integration with how decisions get made — and that's precisely where most ERM programs either prove their value or quietly stall.

What Does the Research Say: Does ERM Actually Increase Firm Value?

The research answer is yes — but with an important condition: value creation depends on how ERM is implemented, not simply whether it's adopted. Across hundreds of studies, a clear pattern emerges that separates organizations that benefit from those that don't.

The Headline Statistic

The Broadleaf 2026 practitioner review of 212 papers found 194 positive findings (68%) and only 13 negative findings (4.5%) across financial and non-financial firms, multiple geographies, and company sizes. The causal evidence is described as "limited but consistent" — ERM doesn't automatically create value, but well-implemented ERM reliably correlates with stronger performance.

How Researchers Measure Value

Studies use two types of metrics:

| Metric Type | Examples Used in Research | Relevance for Private Businesses |

|---|---|---|

| Market-based value | Tobin's Q, stock price premium | Less directly applicable |

| Earnings-based value | ROA, ROE, cash flow, cost efficiency | Directly relevant |

For privately owned businesses, the most meaningful metrics are earnings stability, cost of capital, and long-term profitability — all of which ERM has been shown to improve.

What Specific Studies Found

- Hoyt and Liebenberg (2011) found U.S. insurers with ERM programs traded at roughly a 20% value premium compared to non-ERM peers

- In Taiwanese financial firms, ERM adoption added 5.37% to firm value, improved revenue efficiency by 9.22%, and cost efficiency by 16.34% — per Chen et al. (2020)

- Pan et al. (2023) studied 8,386 observations from Chinese manufacturing firms and found a statistically significant positive relationship between ERM adoption and Tobin's Q

The Important Nuance

Not every study confirms value creation. McShane, Nair, and Rustambekov found that merely reaching an ERM label — without meaningfully exceeding traditional risk-management capability — produced no additional value. Tahir and Razali found neutral Tobin's Q results for Malaysian ERM adopters. Anton (2018) found ERM showed a pre-crisis premium in Romanian firms but no significant effect across the full period including the financial crisis.

The pattern across these studies is consistent: ERM creates value when it genuinely improves how an organization identifies and manages risk — not when it's treated as a compliance checkbox.

Maturity Over Time

Callahan and Soileau's research found that ERM process maturity — not just adoption — is positively associated with industry-adjusted ROA and ROE. Early-stage programs often show modest or neutral results. The performance gains compound for organizations that build and sustain ERM discipline over time — making patience and consistency core to any successful implementation.

How ERM Creates Value: The Five Mechanisms

Mechanism 1 — Reduced Cost of Capital

Berry-Stölzle and Xu (2018) found that ERM adoption significantly reduces cost of equity capital for U.S. insurers. A separate study of 310 Indonesian nonfinancial companies found effective ERM is associated with lower cost of debt through reduced information asymmetry and greater financial transparency.

Lenders and investors charge more when they can't see how a business manages its risks. ERM makes that picture clearer, which reduces the risk premium they demand.

Mechanism 2 — Improved Earnings Stability

ERM surfaces threats before they cause losses — supply chain disruptions, customer concentration, regulatory changes — and enables the business to respond proactively. Earnings stability matters for valuation because:

- Banks price credit on earnings predictability

- Buyers apply higher EBITDA multiples to businesses with consistent cash flows

- Partners and suppliers extend better terms to businesses they trust to remain solvent

Mechanism 3 — Stronger Strategic Decision-Making

Jabbour and Abdel-Kader (2015) found that ERM adoption drives movement toward risk-adjusted performance measures, improving how businesses allocate capital. ERM gives leadership a clearer picture of which opportunities carry manageable risk and which carry disproportionate exposure. The result shows up in three ways:

- Fewer costly expansion mistakes from mispriced risk

- Better capital allocation toward higher-return opportunities

- Faster identification and exit from underperforming investments

Mechanism 4 — Enhanced Stakeholder Confidence

Visible, credible risk management shifts how every major stakeholder interacts with the business:

- Creditors extend better financing terms due to lower perceived default risk

- Customers make longer-term commitments when they trust operational continuity

- Employees accept roles with more confidence — and sometimes at competitive rather than premium compensation

Each of these effects touches the income statement directly. Together, they compound — lower financing costs, longer customer contracts, and reduced hiring premiums all hit profitability simultaneously in ways that isolated risk tools can't replicate.

Mechanism 5 — Operational Efficiency Gains

ERM surfaces process vulnerabilities and compliance gaps that would otherwise go unnoticed until they become expensive. Callahan and Soileau's research links ERM process maturity directly to improved operating ROA and ROE. The Chen et al. study's finding of a 16.34% cost efficiency improvement in ERM-adopting firms reflects this dynamic — organizations that identify and address operational gaps proactively avoid the far steeper costs of reactive damage control.

When ERM Doesn't Increase Value (And How to Avoid Those Pitfalls)

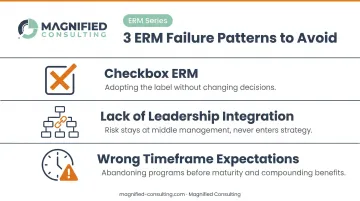

The research is equally clear about when ERM fails. Three patterns appear consistently.

Pitfall 1: Checkbox ERM

McShane et al.'s finding is worth repeating: businesses that simply reach an "ERM label" without exceeding their existing risk management capability see no value improvement. Appointing a risk officer, building a risk register, and scheduling quarterly reviews without connecting any of it to real decisions generates reporting costs with no performance benefit.

ERM creates value when it changes how decisions get made. If the operational process stays the same, the financial outcomes will too — which is why Pitfall 2 is about where ERM actually needs to live.

Pitfall 2: Lack of Leadership Integration

Gordon, Loeb, and Tseng (2009) found that ERM performance depends on how well it fits the organization across five dimensions:

- Uncertainty and risk exposure

- Competitive environment

- Organizational size and complexity

- Board monitoring and governance

ERM that exists at the middle-management level but never enters strategic conversations about expansion, capital allocation, or major contracts rarely produces measurable value.

Pitfall 3: Wrong Timeframe Expectations

Businesses new to structured risk management often see modest or neutral results in the first year. Expecting immediate ROI leads to early abandonment before the program matures. ERM maturity and value creation compound. Abandoning a program at 18 months because results aren't visible yet is one of the most common and costly ERM mistakes.

Applying ERM in Privately Owned and Family-Run Businesses

A common assumption is that ERM belongs to large publicly traded corporations with dedicated risk committees and Chief Risk Officers. The research doesn't support that assumption.

Syrova and Spicka (2022) studied 296 Czech nonfinancial SMEs and found that ERM affects financial performance — through organizational culture and strategic risk management — in smaller, privately held companies as well. The mechanisms are the same; the infrastructure required is not.

What Scalable ERM Looks Like for a $10M–$100M Business

You don't need a CRO. You need a structured process for answering a few essential questions:

- What are the 4–6 risks most likely to disrupt revenue or reduce business value? Common examples include key person dependency, customer concentration, supply chain fragility, and regulatory exposure

- Which of those risks are currently unmanaged or undermanaged?

- How do those risks connect to strategic decisions the leadership team is already making?

That conversation, held consistently with the right people involved, is the foundation of scalable ERM. Magnified Consulting works with privately owned businesses across manufacturing, construction, retail, and professional services to identify operational, financial, and regulatory risks — then build mitigation plans tied directly to business performance.

The M&A and Exit Dimension

For owners considering a sale, recapitalization, or succession plan, ERM has a direct impact on what a buyer will pay. Based on Magnified Consulting's experience advising on over $1.5 Billion in M&A transactions, buyers apply valuation discounts when they find:

- Unresolved contingent liabilities or tax exposure

- Heavy owner dependency with no succession depth

- Compliance gaps in regulated industries

- Inconsistent financial records that obscure true earnings

A business that has already identified and addressed these risks enters a transaction with less uncertainty, which translates directly into a lower discount applied to enterprise value. For non-listed firms, acquisition offers hinge on EBITDA multiples, earnings stability, and customer and employee retention. Structured risk management influences all three.

Frequently Asked Questions

What are the benefits of enterprise risk management?

ERM reduces earnings volatility, improves strategic decision-making, lowers cost of capital, and builds stakeholder confidence with creditors, customers, and employees. The combined effect, when ERM is genuinely integrated into operations, is a measurable improvement in firm value over time.

What are the four pillars of enterprise risk management?

The current COSO ERM framework identifies five components: Governance and Culture; Strategy and Objective-Setting; Performance; Review and Revision; and Information, Communication, and Reporting. Each reinforces the others, with governance setting the tone and reporting keeping leadership informed.

Does ERM work for small and medium-sized businesses?

Yes. Research on SMEs, including a study of 296 Czech nonfinancial SMEs, confirms positive ERM-performance relationships in smaller companies. Scalable ERM doesn't require a large team — it requires a structured, consistent process for identifying and managing the risks most relevant to the specific business.

How is ERM different from traditional risk management?

Traditional risk management addresses isolated risks within specific functions — IT security, safety compliance, financial controls. ERM takes an enterprise-wide view, connecting risk awareness to strategy and leadership decisions across the whole organization.

How long does it take to see results from ERM?

Research links ERM maturity, not just adoption, to performance improvement. Early programs often show modest results. Substantial value creation typically emerges once ERM is embedded in strategic planning and capital allocation — a process that takes sustained effort over multiple years.

What makes an ERM program fail to increase firm value?

The three main failure modes are: treating ERM as a compliance checkbox without integrating it into actual decisions, lacking genuine leadership commitment so risks are identified but never acted on, and abandoning the program before long-term benefits materialize. The research is consistent: the label alone creates no value — only genuine implementation does.