Without documented, repeatable processes, even the most capable advisors find themselves reinventing the wheel before every client meeting, losing hours to administrative tasks, and watching referral opportunities slip through the cracks.

This article covers the five core processes every advisory practice must manage, how to build workflows that actually hold up under growth, the technology stack that ties it all together, and how to know when outside expertise can unlock gains your internal team can't reach alone.

Key Takeaways

- Documented workflows can be delegated, automated, and improved; undocumented routines can do none of those things.

- Five core process categories drive every advisory practice: onboarding, financial planning, investment management, compliance, and client communication.

- 91% of financial advisors now use a CRM, making it the foundational tool for operational efficiency.

- Client retention at high-performing RIA firms holds at 97% — a benchmark worth tracking against.

- When internal KPIs stall, outside expertise moves the needle faster than incremental fixes.

Core Business Processes Financial Advisors Manage

Most advisory practices run on five interconnected process categories. Each feeds the next: poor onboarding creates planning gaps, planning gaps create compliance exposure, and compliance exposure erodes the client trust that drives referrals.

Treating these categories as a system — rather than isolated tasks — is what separates practices that scale from those that stall.

Client Onboarding and Relationship Setup

Onboarding is where first impressions become lasting ones. A well-structured onboarding process runs from the moment a prospect books a meeting through the completion of their financial profile, with zero improvisation along the way.

A structured onboarding sequence typically includes:

- Pre-meeting outreach — Send a welcome email, set expectations, and collect preliminary financial data before the first meeting

- Needs assessment — Conduct a structured discovery conversation covering goals, risk tolerance, current financial position, and concerns

- Data gathering — Use a standardized checklist to collect statements, tax returns, financial policies, and business documents

- Profile completion — Document findings in the CRM and assign follow-up tasks with deadlines

- Follow-up sequencing — Automate 30-, 60-, and 90-day touchpoints to reinforce the relationship and gather missing information

Consistency here matters more than most advisors realize. Cerulli's research found that 80% of clients are satisfied with their primary advisor, yet 55% of advisors identify new client acquisition as a major challenge — a gap that inconsistent early experiences directly widens.

Financial Planning and Analysis Process

The CFP Board's Practice Standards Reference Guide defines a seven-step financial planning process that every advisor should treat as a documented framework, not a loose mental checklist:

- Understand the client's personal and financial circumstances

- Identify and select goals

- Analyze the current course of action and alternatives

- Develop recommendations

- Present recommendations

- Implement recommendations

- Monitor progress and update

For business owner clients specifically, this process demands a dual-track approach. Exit Planning Institute research shows that 80–90% of a business owner's net worth is tied to their business value. Yet only 20–30% of businesses that go to market actually sell — even though 78% of U.S. small business owners plan to fund more than 60% of retirement through a sale.

Advisors who document a dual-track process — one that connects personal financial planning to business value and exit readiness — give those clients a concrete path forward rather than an optimistic assumption.

Compliance and Reporting Workflows

Compliance may not be where advisors prefer to spend their time, but the cost of neglecting it is concrete and well-documented.

SEC-registered investment advisers are required to maintain written policies and procedures, designate a Chief Compliance Officer, and conduct annual compliance reviews. The consequences of gaps are concrete: SEC FY2024 enforcement actions included recordkeeping cases resulting in more than $600 million in civil penalties against more than 70 firms.

Documented compliance workflows reduce this risk across three areas:

- Regulatory filings — Scheduled, assigned, and tracked with deadline alerts

- Documentation standards — Templates and checklists that ensure consistency across all client files

- Client disclosures — Triggered automatically at onboarding and whenever material changes occur

Compliance documentation is a regulatory baseline. Practices that treat it as a secondary concern — something to address after client work — are the ones that show up in enforcement reports.

How to Build and Optimize Efficient Advisor Workflows

There's a real difference between having a routine and having a workflow. A routine lives in someone's head. A workflow is documented, assigned, and repeatable: it survives staff turnover, scales with growth, and can be improved without starting from scratch.

Think of it as the operations manual for your practice. If it only exists because one person remembers to do it, it isn't a system.

Step 1 — Document the Process Before Automating It

The most common mistake advisors make is jumping straight into their CRM without first mapping the process manually. Start on a whiteboard or a simple Word document. List every step, who does it, and how long it should take.

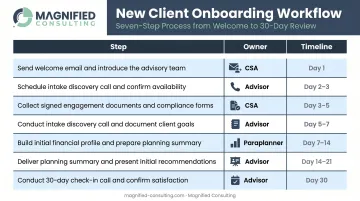

For a new client onboarding workflow, that might look like:

| Step | Owner | Timeline |

|---|---|---|

| Send welcome email and data request | CSA | Same day as booking |

| Confirm meeting and send prep checklist | CSA | 3 days before meeting |

| Conduct discovery meeting | Advisor | Day 1 |

| Document findings in CRM | Paraplanner | Within 24 hours |

| Draft financial profile summary | Paraplanner | Within 5 business days |

| Schedule follow-up meeting | CSA | Day 7 |

| Send 30-day check-in | CSA | Day 30 |

This exercise surfaces missing steps and redundancies before they're locked into a system that's costly to untangle later.

Step 2 — Assign Roles and Build Accountability

Every step in a workflow needs a clearly designated owner. Not "the team." Not "whoever is available." A specific role with a defined timeline.

Unassigned tasks are the primary reason items fall through the cracks in growing advisory firms. When two people assume the other is handling something, nobody handles it. Role clarity removes that ambiguity and makes performance reviews considerably more straightforward.

Step 3 — Automate Through Your CRM

Once the process is tested and refined on paper, migrate it into your CRM as a workflow with:

- Automatic task triggers when a new client record is created

- Deadline alerts assigned to specific team members

- Status indicators that surface overdue items before they escalate

This is what transforms a one-time documentation effort into a scalable, repeatable system. The CRM does the reminding; your team does the work.

Step 4 — Review, Gather Feedback, and Refine

Workflows require maintenance. Schedule quarterly or annual reviews of each core workflow, ask team members where friction occurs, and gather client feedback — through direct conversation or brief surveys — about where the process feels unclear.

Common friction signals worth watching:

- The same step gets skipped repeatedly

- Team members create their own workarounds

- Clients ask the same question at the same point in the process

- Tasks consistently miss deadlines

Any of these patterns signals it's time to revisit the workflow — not assume the team needs to try harder.

Technology Tools That Power Streamlined Operations

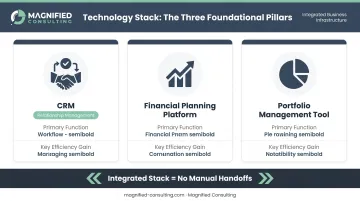

Every advisory practice needs three foundational technology categories working together:

| Tool Category | Primary Function | Key Efficiency Gain |

|---|---|---|

| CRM | Workflow management, relationship tracking | Automates task sequences, reduces manual follow-up |

| Financial Planning Platform | Goal tracking, analysis, client portals | Centralizes client data, eliminates re-entry |

| Portfolio Management Tool | Investment oversight, reporting | Automates performance reporting, flags drift |

When these three tools integrate, manual handoffs disappear. Data entered once flows across the stack — no re-keying, no version mismatches.

CRM adoption among advisors has reached 91.08%, according to the 2026 T3/Inside Information Software Survey, making it the clearest baseline for practice operations. Cerulli found that advisors most often credit e-signature (65%) and CRM (44%) with improving operational efficiency — but also that 29% of advisors say managing their technology needs remains one of their greatest practice challenges. High adoption rates don't equal high utilization. Owning the right tools matters far less than actually building workflows around them.

When evaluating any technology addition, apply three criteria:

- Reduces time on a specific task in a measurable way

- Supports your service models and fee structures without workarounds

- Scales to handle complexity as clients' financial situations grow

Beware of tools that solve 90% of your needs but fail at the critical 10%. That gap tends to grow. For advisors whose current stack has gaps in portfolio management, a Turnkey Asset Management Platform (TAMP) can fill that role — providing technology, marketplace access, and investment management support without requiring advisors to build or maintain it themselves.

Measuring Process Success and Knowing When to Improve

Workflow changes only deliver results if you're tracking whether they actually work. Define the right metrics upfront — then measure before and after every significant process change.

Core KPIs for advisory operations:

- Client retention rate — High-performing RIA firms report 97% retention (Schwab, 2024); a significant gap below that warrants a closer look

- New client acquisition rate — Tracks pipeline health and referral effectiveness

- Meeting-to-close ratio — Kitces research suggests a healthy middle tier converts 25–50% of qualified prospects

- Revenue per client — Indicates whether your service model matches client complexity

- Net Promoter Score — Captures client willingness to refer; relevant to organic growth strategy

- Operational cost per client — Helps identify scale inefficiencies as headcount and client count grow

Build a simple review cadence:

- Monthly — Team review of active workflows: what's on track, what's delayed, what needs a fix

- Quarterly — Deep-dive on client experience metrics and workflow performance data

- Annually — Full operations model review tied to business planning; assess whether core processes still fit the practice's size and complexity

Following this cadence consistently shifts a practice toward identifying friction points early, before they reach clients or create staff bottlenecks.

Common signs a process needs an audit:

- Clients raise the same complaint more than once

- Staff regularly ask which step comes next

- Tasks are frequently missed or handed off late

- What worked smoothly with 50 clients breaks down at 150

Kitces research estimates advisor meeting capacity at roughly 100–150 clients seen three times per year. Growth past that threshold without upgraded processes creates a hard ceiling — one that adding staff alone won't resolve.

When Outside Expertise Transforms Your Operations

Internal process improvements have a natural ceiling. At some point, whether due to rapid growth, a looming transition, or metrics that have plateaued despite real effort, the team inside the practice can't see what an experienced outside perspective can identify.

Advisory practices serving business owners hit this ceiling faster than most. Managing multi-entity structures, capital decisions, and business transitions simultaneously creates a level of operational complexity that internal process work simply can't diagnose from the inside.

An experienced business consultant adds value at this stage through a structured operational audit that identifies cost inefficiencies, workflow gaps, and missed profit opportunities, then builds a prioritized roadmap to address them in sequence.

Magnified Consulting structures this type of engagement for privately owned and family-run businesses generating over $10M in revenue. Their team has been involved in over $1.5 Billion in mergers and acquisitions and has advised on $300 million in capital purchasing decisions, which means their operational recommendations are grounded in actual transactional outcomes — not theoretical frameworks. Clients have reported a 40% increase in profits within six months and a 30% reduction in production times that saved millions annually.

The right time to bring in outside expertise:

- The practice is scaling faster than internal processes can support

- A major transition is approaching — acquisition, exit, ownership change, or succession

- KPIs have plateaued despite internal optimization efforts

- Complexity has grown beyond the team's capacity to diagnose objectively

This is a proactive, strategic decision, not a last resort. Practices that bring in outside perspective before complexity peaks enter transitions with systems already in place — and that preparation is usually what separates a smooth handoff from a costly one.

Frequently Asked Questions

What are the 7 steps of financial planning in business?

The CFP Board defines seven steps: understand client circumstances, identify goals, analyze courses of action, develop recommendations, present recommendations, implement the plan, and monitor progress. Advisors apply this same framework to their own practice management and to the business owner clients they serve.

What do financial advisors do for businesses?

Financial advisors help businesses manage cash flow, budgeting and forecasting, tax planning, investment strategy, risk management, and succession or exit planning. In practice, they connect a company's day-to-day financial decisions to its longer-term growth and wealth-building objectives.

What are the most important workflows for a financial advisory practice?

The five core workflows are client onboarding, financial planning, investment management, compliance and reporting, and ongoing client communication. All five should be documented in writing, assigned to specific roles, and reviewed on a regular schedule.

How do I know if my financial advisor business processes need optimization?

Key warning signs include repeated service errors or missed tasks, difficulty scaling without disproportionate headcount additions, client complaints about inconsistent experiences, and team confusion about who owns which responsibilities. Any one of these signals warrants a process audit.

How can technology improve financial advisor business processes?

CRM systems, financial planning platforms, and portfolio management tools reduce manual work, automate routine tasks, and improve data accuracy. The result is more advisor time available for client relationships and strategic work — rather than administrative catch-up.

What is the difference between a financial advisor and a business consultant?

A financial advisor focuses on financial planning, investment management, and wealth strategy. A business consultant like Magnified Consulting takes a broader operational view: identifying inefficiencies, improving workflows, advising on capital decisions, and guiding business transitions to drive long-term profitability across the whole enterprise.