That gap is expensive. Choosing the wrong fee model, underestimating recurring costs, or defaulting to the cheapest option can leave significant money on the table — and no plan for what comes next.

This article breaks down 2026 pricing by fee structure and service tier, the key factors that push costs higher, a one-time vs. ongoing cost breakdown, and how to budget for planning that actually matches your business complexity.

Key Takeaways

- Financial planning fees range from ~$2,926 for a one-time plan to $6,815+/year for an ongoing retainer, with business complexity routinely pushing costs toward the upper end

- Retainer and subscription fees have surged since 2023; this is now the dominant model for ongoing advisory relationships

- AUM-based pricing often fits poorly when business wealth is illiquid — flat fee or retainer structures typically serve owners better

- Eight in 10 small business owners say financial professionals drive smarter decisions; those with advisors expect to retire seven years earlier

- Underpaying for financial advice typically costs more in missed tax savings, poor exit timing, and unchecked risk than the advisory fee itself

How Much Does Financial Planning Cost for Small Businesses?

Small business financial planning has no fixed price tag. What you pay depends on the fee model, the provider, and the complexity of your situation — and in 2026, all of those costs are trending upward.

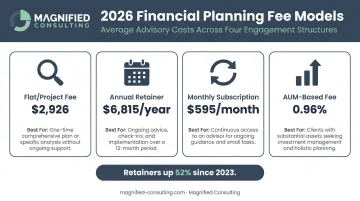

Typical Cost Ranges by Fee Structure

According to Envestnet's 2026 advisor survey, the current benchmarks across fee models are:

| Fee Model | 2026 Average | Best Suited For |

|---|---|---|

| Flat/project fee | $2,926 per plan | One-time planning engagements |

| Annual retainer | $6,815/year | Ongoing advisory relationships |

| Monthly subscription | $595/month | Continuous access, flexible model |

| AUM-based fee | 0.96% of assets managed | Investment-heavy portfolios |

These are general advisor benchmarks — not small-business-only pricing. Business owners with higher complexity, multiple entities, or succession planning needs should expect fees toward the higher end of each range.

Annual retainers jumped 52% since 2023 (from $4,484 to $6,815), and monthly subscriptions nearly tripled (from $215 to $595). The market has shifted decisively toward ongoing planning relationships, not one-time documents.

That shift makes fee model selection more consequential than ever — choosing the wrong structure can leave you paying for coverage that doesn't match how your business actually operates.

Why Fee Model Selection Matters

Picking the wrong fee structure can leave you underserved:

- AUM-based pricing assumes liquid, managed investments — but most small business owners hold wealth in the business itself, equipment, or home services businesses. That makes AUM billing a poor fit for the advisory you actually need

- One-time flat fee plans work for an initial financial checkup but won't evolve with your business

- Owners navigating growth, hiring, capital decisions, or exit prep get more value from retainer or subscription models — higher annual cost, but continuous decision support throughout

What Service Tier Do You Actually Need?

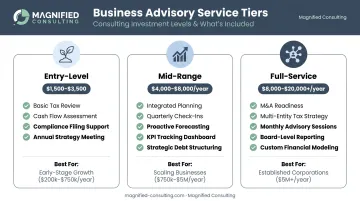

Entry-Level: Basic Financial Planning

Typical cost: $1,500–$3,500 (one-time or hourly)

What's included:

- Basic tax planning review

- Cash flow assessment

- Simple retirement account guidance (SEP-IRA or Solo 401k)

- Minimal ongoing support

Best for: Solo operators, early-stage businesses, or owners seeking a one-time financial checkup rather than continuous guidance.

Mid-Range: Comprehensive Planning

Typical cost: $4,000–$8,000/year (retainer or subscription)

What's included:

- Integrated business and personal financial planning

- Proactive tax strategy

- Cash flow optimization

- Risk and protection planning review

- Quarterly or semi-annual advisor check-ins

Best for: Growing businesses with $1M–$10M in revenue where financial complexity is increasing across tax, cash flow, and operations.

Full-Service: Strategic Financial Planning

Typical cost: $8,000–$20,000+/year

What's included:

- Integrated business financial strategy across operations, tax, and capital

- Capital allocation planning

- M&A readiness or succession planning

- Multi-entity tax strategy

- Ongoing strategic advisory relationship

Best for: Established businesses generating $10M+ in revenue that need a strategic partner — not just a written financial plan. This tier covers the decisions that carry the most financial weight: ownership transitions, capital deployment, and multi-entity tax exposure.

Key Factors That Affect the Cost of Financial Planning

Financial planning fees for small businesses are shaped by factors well beyond what an individual investor would encounter.

Business Size and Revenue Complexity

A business generating $2M in revenue with clean books and a single entity requires far less planning time than one generating $15M+ with multiple revenue streams, employee retirement plans, and cross-entity tax exposure.

Higher revenue typically means:

- More complex tax strategy requirements

- Greater need for cash flow and capital allocation planning

- Broader risk and protection planning considerations

- Succession or exit planning that adds significant scope

Businesses whose wealth is concentrated in the company itself, rather than liquid investment accounts, also tend to fit the AUM model poorly, making flat fee or retainer structures the more practical choice.

Scope of Services Required

The range of financial planning a small business may need is wide:

- Cash flow management and forecasting

- Business tax strategy and entity structure optimization

- Retirement plan setup and management

- Key-person risk planning

- Owner compensation structuring

- Succession or exit planning

- Capital investment planning

Each added service area increases total cost. The more important distinction, though, is between transactional services (a one-time plan, a tax return) and strategic advisory relationships (ongoing retainer or consulting engagement). The latter costs more annually but typically delivers significantly higher ROI when the stakes are high.

Exit and Succession Planning Needs

Exit and succession planning ranks among the highest-cost — and highest-value — financial planning services for business owners. The data makes a compelling case for prioritizing it.

According to the Exit Planning Institute, only 20% to 30% of businesses that go to market actually sell, leaving most owners without a viable path to harvest their wealth. Yet only 32% of owners have a documented exit plan, and just 22% have aligned their personal, business, and financial goals.

CEPA-credentialed advisors and business consultants specializing in exit planning command higher fees, but structured preparation can increase business valuation before a sale — often by more than the advisory cost itself. Exit plan engagements typically range from $7,500 to $50,000 depending on complexity.

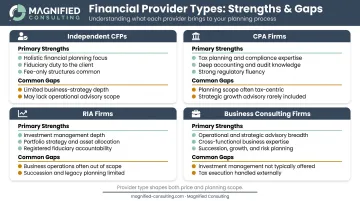

Geographic Location and Provider Type

Fees vary by region. Providers in Southeast markets like Charlotte, South Carolina, Columbia, Myrtle Beach, and Savannah may price differently than national firms, though the service model matters more than geography.

Provider type also shapes both price and scope:

| Provider Type | Primary Strengths | Common Gaps |

|---|---|---|

| Independent CFPs | Investment management, personal retirement planning | Limited business strategy depth |

| CPA Firms | Tax compliance, accounting | Less focus on operational or capital planning |

| RIA Firms | Portfolio and investment management | May not address growth or exit readiness |

| Business Consulting Firms | Capital strategy, operational efficiency, exit planning | Varies by firm; less investment-focused |

Understanding these four factors together — revenue complexity, service scope, exit planning needs, and provider type — gives you a framework for evaluating both what you need and what you should expect to pay.

Complete Cost Breakdown: One-Time vs. Ongoing Expenses

The total cost of financial planning goes beyond any single engagement. Business owners should budget across both categories:

| Service | Type | Typical Cost Range |

|---|---|---|

| Initial financial plan / diagnostic | One-time | $2,500–$5,000 |

| Tax strategy planning session | Annual or one-time | $1,500–$5,000+ |

| Ongoing retainer / advisory relationship | Recurring | $6,000–$15,000/year |

| Succession or exit planning engagement | Project-based | $7,500–$50,000 |

| Retirement plan setup and annual management | Recurring | $1,000–$3,000+/year |

Businesses approaching a major transition — a capital raise, acquisition, or ownership exit — should plan for costs on the higher end of these ranges. These engagements typically involve business valuation work, multi-stakeholder coordination, and legal alignment that add time and specialized expertise to the process.

What Small Business Owners Get Wrong About Financial Planning Costs

Treating Planning as an Expense, Not an Investment

The ROI framing matters here. Survey data from Equitable and SCORE found that eight in 10 small business owners working with financial professionals report making smarter business decisions — and those with advisors expect to retire seven years earlier than those without.

Tax savings, improved capital allocation, and higher business valuations at exit routinely return multiples of the advisory fee. The math only looks unfavorable if you're comparing the fee to nothing rather than to the alternative outcomes.

Waiting Until a Crisis

Timing is part of what determines whether that investment pays off. The highest-value financial planning is proactive:

- Building tax strategy before year-end (not after)

- Preparing for an exit well in advance of going to market

- Structuring capital decisions before they become urgent

Reactive planning is more expensive and less effective. By the time a problem forces a decision, the planning options narrow and the cost of poor decisions grows.

Confusing Cheapest with Best Value

A low hourly rate or an inexpensive online financial plan won't address entity structure, succession planning, or owner compensation — the issues that actually move the needle for a small business owner. Look for an advisor with direct experience in those areas, not just general financial credentials.

How to Estimate the Right Financial Planning Budget

The right budget isn't the lowest available price. It's determined by the complexity of your business, the stakes of upcoming decisions, and the ROI you expect from professional guidance.

Build your budget around these factors:

- Businesses with $10M+ in revenue, multiple entities, or significant business-tied assets need ongoing advisory relationships, not one-off plans

- Capital raises, equipment purchases, acquisitions, and ownership transitions all warrant higher planning investment — the cost of a mistake far exceeds the advisor fee

- Many owners are business-rich but personally asset-poor, with enterprise value built up while personal wealth stays undiversified; integrated planning addresses both sides

For owners at the $10M+ revenue level, financial planning needs go beyond standard advisory work. Capital allocation, operational efficiency, business transitions, and exit readiness all require coordinated strategy — not isolated advice.

Firms like Magnified Consulting specialize in exactly this. With involvement in over $1.5 Billion in M&A transactions and $300 million in capital purchasing decisions, the team ties planning directly to measurable growth and profitability outcomes.

Frequently Asked Questions

What is a reasonable fee for financial planning?

Reasonable fees depend on scope. In 2026, a standalone financial plan averages around $2,926, and ongoing annual retainers average $6,815. Small business financial planning typically runs higher than individual planning due to added complexity in tax strategy, entity structure, and succession considerations.

How much should a small business budget for financial planning each year?

Most small businesses should budget between $3,000 and $15,000 annually, depending on revenue, complexity, and whether they need continuous advisory support or periodic project-based planning. Businesses approaching an exit or major capital decision should budget toward the higher end.

What is the difference between a financial planner and a business consultant?

Financial planners typically focus on investment management, tax planning, and retirement strategy. Business consultants address broader strategic issues including capital allocation, operational efficiency, growth planning, and exit readiness. Many business owners benefit from both, or from working with a firm that covers both disciplines.

When is the right time to hire a financial planner?

The right time is before a major financial decision — a capital raise, ownership transition, significant equipment purchase, or exit — or when business complexity outpaces your ability to manage it effectively. For exit planning specifically, engaging well in advance gives you time to improve valuation before going to market.

Is a CFP better than a CPA for small business financial planning?

CPAs specialize in tax compliance and accounting; CFPs focus on broader financial planning including investments and retirement strategy. The best fit depends on your primary need. Many business owners find the most value in a team approach — or in professionals who hold both credentials.

Is $200,000 enough to work with a financial advisor?

$200,000 in investable assets qualifies for many AUM-based advisors. But for small business owners whose wealth is concentrated in the business rather than liquid accounts, fee-for-service or retainer-based models are typically a better fit — regardless of investable asset levels.